커뮤니티

문의

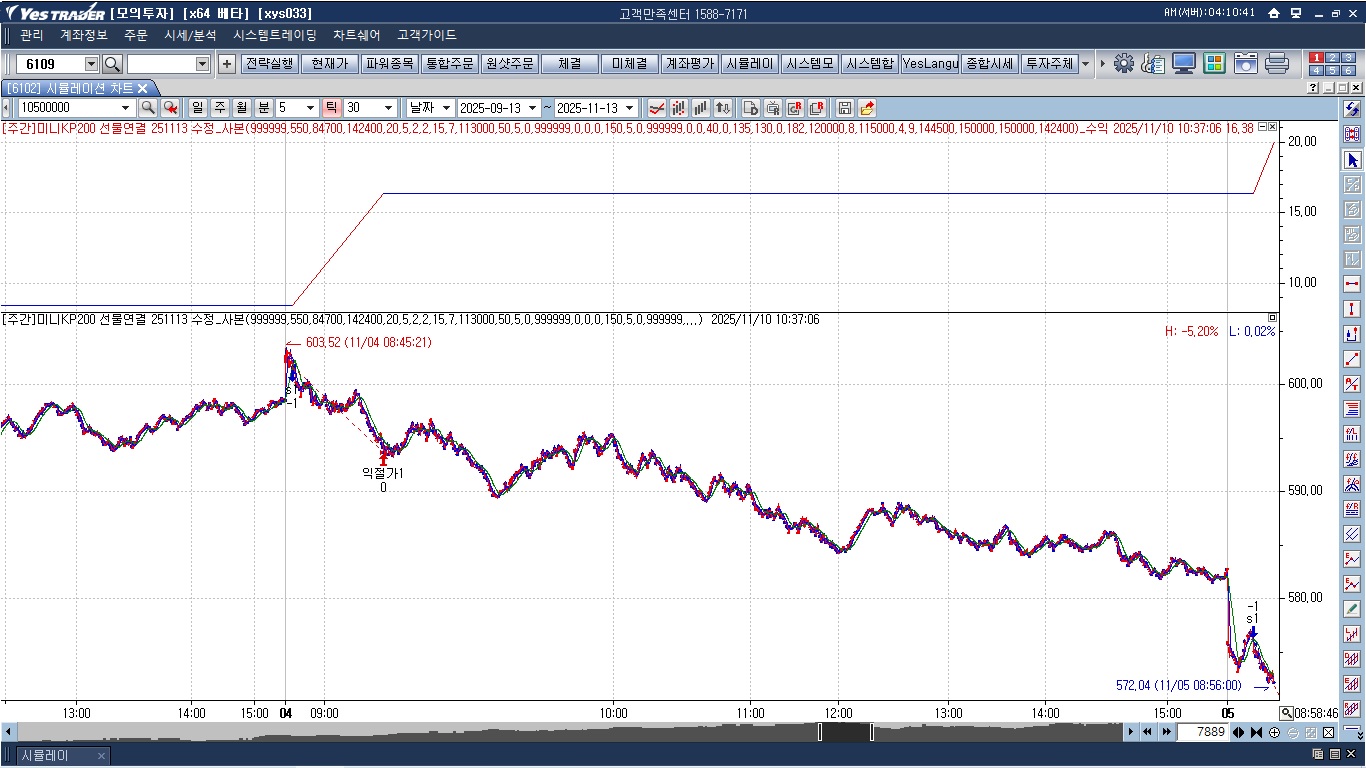

첨부 이미지

sell 수식에서 익절 발생 후 그 이후 진입은 익절가보다 낮은 가격에서 진입하도록

수식을 수정했는데...익절가 발생 후 부터는 아예 진입을 하지 않는 수식이 되었습니다.

살펴주십시요.

첨부파일 1은 기존 수식 결과

첨부파일 2는 수정 수식 결과

***************************************************************************************************************************

input : 최대(999999),최소(550);

input : 진입시간(084700),진입제한시간(142400);

input : 거래횟수(20),누적패수(5),연속패수(2),누적패수조정(2),bigdown(15.00),조정거래횟수(7),조정진입제한시간(113000);

input : b1(50),진입눌림1(5),진입돌파1(0),X1(999999),청산눌림1(0),청산돌파1(0);

input : 경과봉(0),b2(150),진입눌림2(5),진입돌파2(0),X2(999999),청산눌림2(0),청산돌파2(0);

input : als(40),atr1(0),atr2(135);

input : bls(130),btr1(0),btr2(182);

input : s1lock(120000),익절가1(8);

input : s2lock(115000),익절가2(4.9);

input : 만기청산시간1(144500),만기외청산시간1(150000);

input : 만기청산시간2(150000),만기외청산시간2(142400);

var : T1(0),entry(0),HH(0),LL(0),EH(0),EL(0),E1(0),H1(0),i1(0),S1(0),L1(0),V1(0);

Var : 당일거래횟수(0),진입끝시간(0),bigdownCond(False);

var : Tcond(false);

var : loss(0),consecLoss(0),패수(0),익절가(0);

//영업일변경

if bdate != bdate[1] Then

{

//손실횟수 초기화 0

loss = 0;

//연속손실횟수 초기화 0

consecLoss = 0;

//패수는 누적패수

패수 = 누적패수;

//익절1이나 익절2가 발생하면 청산가격 저장할 변수

익절가 = 0;

}

//청산발생

if TotalTrades > TotalTrades[1] Then

{

//손실이면

if PositionProfit(1) < 0 Then

{

//loss 1씩 증가

loss = loss+1;

//consecLoss 1씩 증가

consecLoss = consecLoss+1;

//consecLoss이 3이면 패수를 누적패수에서 누적패수조정으로 변경

if consecLoss == 연속패수 Then

{

패수 = 누적패수조정;

}

}

Else //손실이 아니면 consecLoss으로 초기화

consecLoss = 0;

//청산으로 익절1이나 익절2이면 익절가에 청산가격 저장

if IsExitName("익절1",1) == true or IsExitName("익절2",1) == true Then

익절가 = ExitPrice(1);

Else // 아니면

익절가 = 0; //익절가는 0

}

//영업일 변경

if bdate != bdate[1] Then

{

//손실횟수 초기화 0

loss = 0;

//연속손실횟수 초기화 0

consecLoss = 0;

//패수는 누적패수

패수 = 누적패수;

//당일거래횟수는 거래횟수

당일거래횟수 = 거래횟수;

//진입끝시간은 진입제한시간

진입끝시간 = 진입제한시간;

//bigdownCond는 False

bigdownCond = False;

}

//bigdownCond가 False인 상태에서

//진입시간이후 조정진입제한시간 전에 시초가대비 BigDown이하 하락한 종가가 발생하면

if bigdownCond == False and

stime >= 진입시간 and sTime < 조정진입제한시간 and

L <= DayOpen-BigDown Then //전일종가대비이면 DayOpen-> DayClose(1)

{

//BigDown는 true

bigdownCond = true;

//당일거래횟수는 조정거래횟수로 변경

당일거래횟수 = 조정거래횟수;

//진입끝시간은 조정진입제한시간로 변경

진입끝시간 = 조정진입제한시간;

//진입제한시간이후에 발생했다면 Tcond가 False이므로

//Tcond는 true로 변경

if sTime >= 진입제한시간 and Tcond == False Then

Tcond = true;

}

if TotalTrades > TotalTrades[1] and PositionProfit(1) < 0 Then

loss = loss+1;

if (sdate != sdate[1] and stime >= 진입시간) or

(sdate == sdate[1] and stime >= 진입시간 and stime[1] < 진입시간) Then

Tcond = true;

if (sdate != sdate[1] and stime >= 진입끝시간) or

(sdate == sdate[1] and stime >= 진입끝시간 and stime[1] < 진입끝시간) Then

Tcond = false;

if (sdate != sdate[1] and stime >= 진입시간) or

(sdate == sdate[1] and stime >= 진입시간 and stime[1] < 진입시간) Then{

T1 = TotalTrades;

E1 = 0;

HH = H;

}

if stime >= 진입시간 then

{

if H > HH Then

HH = H;

if MarketPosition == 0 Then

entry = TotalTrades-T1;

Else

entry = (TotalTrades-T1)+1;

if MarketPosition == 0 and entry == 0 Then

{

if E1 == 0 and C <= HH-PriceScale*B1 Then

{

E1 = 1;

L1 = L;

i1 = index;

V1 = HH; //시작점 종가

}

if E1 == 1 and index > i1 then{

if L < L1 Then

L1 = L;

#고가가 시작봉종가보다 작을 때만 눌림체크

if H <= V1 and H >= L1+PriceScale*진입눌림1 Then{

E1 = 2;

i1 = index;

S1 = L1;

}

}

//시작점 종가보다 높은 가격이 발생하면 초기화

if E1 >= 1 and H > V1 Then{

E1 = 0;

HH = H;

}

if loss < 패수 and E1 == 2 and index > i1 and C <= S1-PriceScale*진입돌파1 and Tcond == true and 최대 > C and C >= 최소 Then{

sell("s1");

}

}

if TotalTrades > TotalTrades[1] Then{

E1 = 0;

HH = H;

}

if H > HH Then

HH = H;

if MarketPosition == 0 and entry >= 1 and entry < 당일거래횟수 Then{

if E1 == 0 and C <= HH-PriceScale*B2 Then{

E1 = 1;

L1 = L;

i1 = index;

}

if E1 == 1 and index > i1 then{

if L < L1 Then

L1 = L;

if H >= L1+PriceScale*진입눌림2 Then{

E1 = 2;

i1 = index;

S1 = L1;

}

}

if loss < 패수 and E1 == 2 and index > i1 and C <= S1-PriceScale*진입돌파2 and Tcond == true and 최대 > C and C >= 최소 and

(익절가 == 0 or (익절가 > 0 and C < 익절가)) Then //익절가가 0이거나 익절가가 0보다 크면 종가가 익절가보다 작다 Then{

sell("s2");

E1 = 0;

}

}

if MarketPosition == -1 and IsEntryName("s1") == true Then{

if entry >= 1 then{

if CurrentContracts > CurrentContracts[1] Then{

EL = L;

E1 = 0;

}

if L < EL Then{

EL = L;

E1 = 0;

}

if E1 == 0 and C >= EL+PriceScale*X1 Then{

E1 = 1;

H1 = H;

i1 = index;

}

if E1 == 1 and index > i1 Then{

if H > H1 Then

H1 = H;

if L <= H1-PriceScale*청산눌림1 Then{

E1 = 2;

I1 = index;

S1 = H1;

}

}

if E1 == 2 and index > i1 and C >= S1+PriceScale*청산돌파1 Then{

ExitShort("sx1");

E1 = 0;

}

}

}

if MarketPosition == -1 and IsEntryName("s2") == true Then{

if entry >= 1 then{

if CurrentContracts > CurrentContracts[1] Then{

EL = L;

E1 = 0;

}

if L < EL Then{

EL = L;

E1 = 0;

}

if E1 == 0 and C >= EL+PriceScale*X2 Then{

E1 = 1;

H1 = H;

i1 = index;

}

if E1 == 1 and index > i1 Then{

if H > H1 Then

H1 = H;

if L <= H1-PriceScale*청산눌림2 Then{

E1 = 2;

I1 = index;

S1 = H1;

}

}

if E1 == 2 and index > i1 and C >= S1+PriceScale*청산돌파2 Then{

ExitShort("sx2");

E1 = 0;

}

}

}

if marketposition() == -1 and IsEntryName("s1") == true and stime<s1lock Then

ExitShort("익절가1",Atlimit,EntryPrice-익절가1);

if marketposition() == -1 and IsEntryName("s2") == true and stime<s2lock Then

ExitShort("익절가2",Atlimit,EntryPrice-익절가2);

if MarketPosition== -1 Then

{

if IsEntryName("s1") == true Then

{

SetStopLoss(PriceScale*als,PointStop);

SetStopTrailing(PriceScale*atr2,PriceScale*atr1,PointStop,1);

}

Else if IsEntryName("s2") == true Then

{

SetStopLoss(PriceScale*bls,PointStop);

SetStopTrailing(PriceScale*btr2,PriceScale*btr1,PointStop,1);

}

Else

{

SetStopLoss(0);

SetStopTrailing(0,0);

}

}

var : Month(0),nday(0),week(0);

month = int(date/100)-int(date/10000)*100;

nday = date - int(date/100)*100;

Week = DayOfWeek(date);

if (nday >= 8 and nday <= 14 and

week == 4) or (sdate == 20141008) then

{

if sdate < 20160801 Then

SetStopEndofday(만기청산시간1);

Else

SetStopEndofday(만기청산시간2);

}

Else

{

if sdate < 20160801 Then

SetStopEndofday(만기외청산시간1);

Else

SetStopEndofday(만기외청산시간2);

}

{kind=link}

{kind=link}

답변 1

예스스탁 예스스탁 답변

2025-11-13 10:49:03